Our 2024 Wish List

As we enter a new year, we consider the following a “wish list”: lower inflation, lower interest rates, higher investment value and, last but not least, peace!

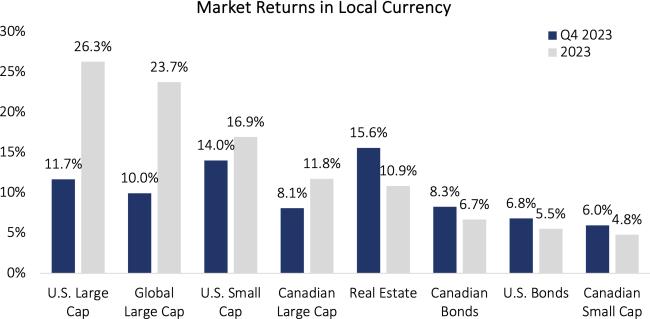

As inflation continues to decline, central banks have signaled their job to battle inflation is almost done and cuts may be coming soon. This change in trajectory ignited a sharp rally in the values of bonds and stocks in the final quarter of 2023 (see the chart below). In certain asset classes (Canadian bonds, U.S. bonds, real estate, Canadian small caps), the Q4 return turned the full year from negative to positive. This once again reminded investors of the importance of staying invested. The U.S. large cap stocks, as measured by the S&P 500 Index, finished the year at 4783, which is 14 points below the all-time-high recorded on January 3, 2022. High inflation seems to be short-lived, along with high interest rates and poor stock performance. So far, it is the consensus that inflation is controlled and rates will be lower as stocks are repricing to represent forward-looking valuations. We will find out if those conditions are met in the coming months of 2024.

Peace is harder to achieve, with at least two ongoing wars and threats of military action by North Korea and China. Yet, we remain hopeful. Our portfolios are generally positioned for the medium to long term rather than the near term. We do have an overweight position in energy due to company-specific valuations and cash flows, but not due to geopolitical concerns. We expect companies to benefit from lowering interest rates, stable economic growth and ongoing innovation.

Speaking of innovation, Apple is expected to launch its Vision Pro headset in the first quarter. This may be the next “hot” gadget to own after the iPod, iPad, iPhone and Apple Watch. Its failure or success will have a direct and significant impact on the S&P 500’s performance given Apple’s significant weight in the Index. Innovation has continued to drive stock prices higher in the U.S., against traditional wisdom that the performance is all due to the economy. Innovation is hard and fierce in competing for dominance in artificial intelligence (AI). The largest technology giants have all committed to spending on AI initiatives, and that’s hundreds of billions of dollars. This unfortunately leaves small cap companies out of the game. AI chip maker Nvidia is busier than ever trying to meet demand and also upgrading their products to compete. We will hear more as these companies report their Q4 earnings, which will allow us to reassess the “speed of change”. 2024 is set up to be interesting, with less restrictive monetary policies and innovation that may exceed your imagination.

Summary

Central banks have begun to signal that interest rate cuts may be imminent, which already spurred a rally in Q4 of 2023, particularly for Canadian and U.S. bonds, real estate, U.S. large caps, and Canadian small caps. Many believe that lower inflation, lower interest rates, and higher investment values are just around the corner, but only time will tell. Geopolitical concerns could detract from economic stability in 2024, while tech advancements could generate significant value.

About the Author

Alfred has more than 18 years of experience specializing in portfolio design, asset allocation, manager and fund selection, and risk management. While at CI Global Asset Management, Alfred has brought unique ideas and processes to the management of the team’s multi-asset strategies, including a mean-reversion currency management strategy, the concept of investing in concentrated and benchmark-agnostic portfolios, and a new approach to risk management. In addition to the Chartered Financial Analyst (CFA) designation, Alfred holds an MBA from the York University Schulich School of Business, and is a member of the CFA Institute and the Toronto CFA Society.

IMPORTANT DISCLAIMERS

The opinions expressed in the communication are solely those of the author(s) and are not to be used or construed as investment advice or as an endorsement or recommendation of any entity or security discussed. This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what CI Global Asset Management and the portfolio manager believe to be reasonable assumptions, neither CI Global Asset Management nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

Certain names, words, titles, phrases, logos, icons, graphics, or designs in this document may constitute trade names, registered or unregistered trademarks or service marks of CI Investments Inc., its subsidiaries, or affiliates, used with permission. All other marks are the property of their respective owners and are used with permission. © 2023 Morningstar Research Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document.