The sun is shining again!

The following is a commentary written by our sub-advisors, Munro Partners, who manage a U.S. equity mandate and a global mandate for our program. They are based in Australia and are known as growth investors.

We understand it's difficult to be optimistic when global economies are slowing, geopolitics are continuously challenging, and many are struggling to pay their monthly mortgage bills. It is worth pausing to reflect on how much investors have endured over the last few years and how we expect to see this improve.

COVID essentially created a vicious economic cycle where otherwise one probably wouldn’t have existed. Interest rates went to zero initially and then rapidly up to 5%. Deflation flipped to rampant inflation and now to disinflation. Many company and business owners had to endure extreme labour and component shortages, only to find that once they finally procured what they needed their customers could no longer afford to buy their products.

All of this is now behind us. We believe interest rates, while high, have peaked for this cycle. Inflation should continue to normalize. Supply chains are open again, and inventories are now being worked through every quarter. The economic outlook is far from rosy, but it is important to remember that central banks have 500 basis points of interest rate cuts up their sleeve, if required. In fact, central banks now see themselves in the strongest position they have been in in a decade, having seemingly normalized interest rates without collapsing the economy. Consequently, this should ultimately enable them to manage a long and sustained economic upswing, which, barring any unforeseen events, should hopefully begin sometime in the second half of 2024. While there may still be some volatility in the near term, we see many reasons to be optimistic in the medium term.

Meanwhile, human innovation has continued, and while investors remain focused on last year’s battles, we see large structural changes occurring in the world that continue to present compelling investment opportunities. This is where we have positioned our funds, not just for 2024 but for the sustained upcycle ahead.

We see AI as having its iPhone moment in 2023. Artificial intelligence has been around since 2017 but was mainly used by large internet players and was expensive to implement. Generative AI or Large Language Models such as Chat GPT have changed everything. Now, AI models can create amazing results and can be seemingly plugged into everything. In the same way that the iPhone made mobile internet work for everyone, generative AI will make AI work for everyone.

It's only been a year since Chat GPT came into many of our lives, and we are already seeing products come to market. GitHub predicts code for developers, making them up to 60% more efficient. Adobe Firefly allows creatives to build pictures from words. Fathom, Otter.AI, and plenty of other applications will be able to listen to and summarize your meetings. Microsoft Co-Pilot is currently predicting each sentence as I try to write this outlook.

We see a global boom brewing here as companies across the globe either invest in developing their own AI tools or invest in protecting themselves against getting disrupted by others’ AI tools. We expect to see a sustained upswing for the shovels in this boom, be it the cloud infrastructure providers or the semiconductor companies that supply them. Large software companies also look uniquely positioned here as they essentially have a whole new way of selling their customers' data back to them. As an example, existing accounting software keeps invoices and accounts in order, but in the future, the software will be able to help with budgeting and planning. While, clearly, these products are not perfect today, we argue that neither was the first iPhone. We see this as just the beginning of a huge investment trend and one that we are positioned to benefit from today and hopefully well into the future.

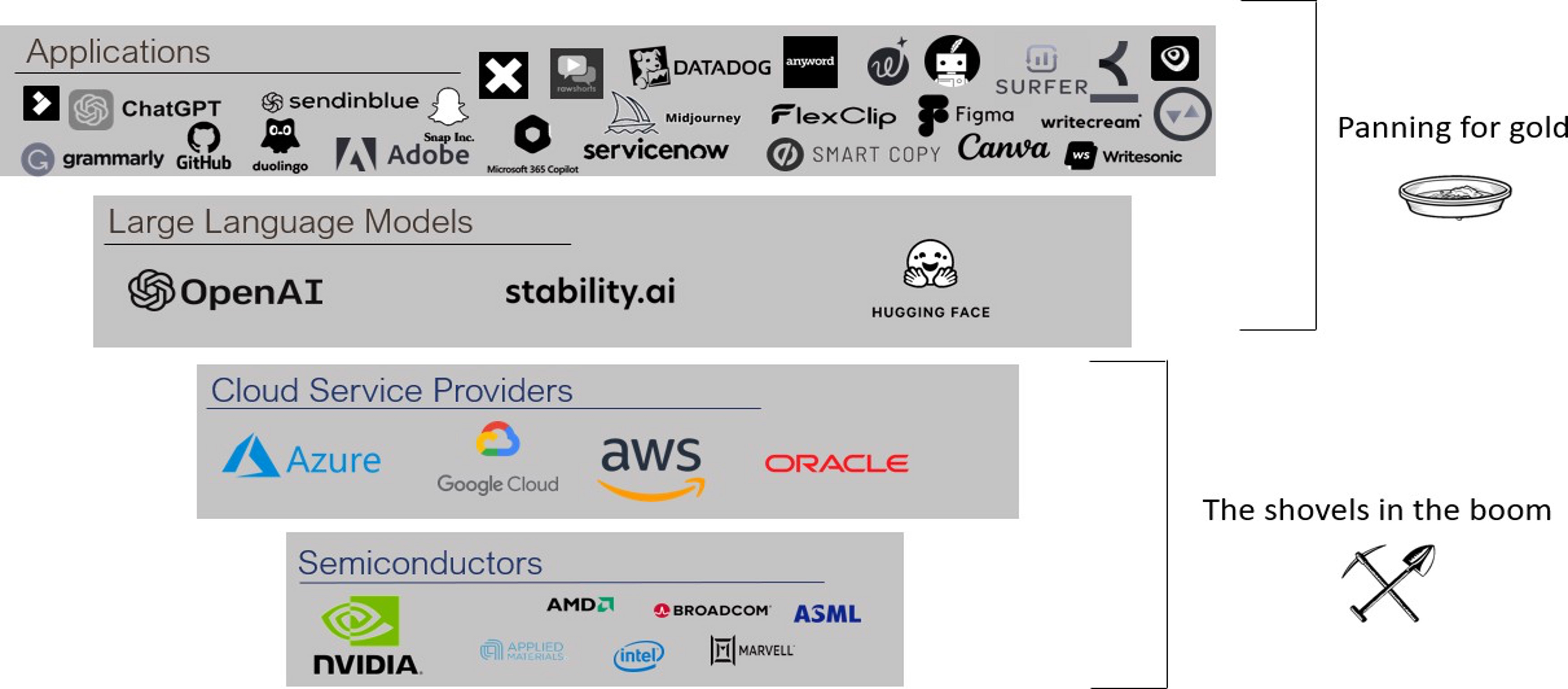

The graphic below is one we have stood behind for the better part of 2023. It depicts our approach to investing in AI, which is focused on the enablers initially as they are uniquely positioned to benefit from the coming wave of adoption. As we enter 2024, exciting products will appear, and we expect to broaden our exposure to newer, application-based ideas that should help sustain the explosive growth in AI seen in just this year alone.

Source: Munro Partners

Summary

Interest rates, while high, have peaked for this cycle, and inflation should continue to normalize. While financial challenges are still affecting consumers, the worst is now behind us and an economic upswing should begin in the second half of 2024, fuelled by significant interest rate cuts. Generative AI represents a standout opportunity that will continue to evolve, with some uniquely positioned companies set to profit more than others.

IMPORTANT DISCLAIMERS

The opinions expressed in the communication are solely those of the author(s) and are not to be used or construed as investment advice or as an endorsement or recommendation of any entity or security discussed. This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what CI Global Asset Management and the portfolio manager believe to be reasonable assumptions, neither CI Global Asset Management nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

Certain names, words, titles, phrases, logos, icons, graphics, or designs in this document may constitute trade names, registered or unregistered trademarks or service marks of CI Investments Inc., its subsidiaries, or affiliates, used with permission. All other marks are the property of their respective owners and are used with permission. ©2024.

Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document.